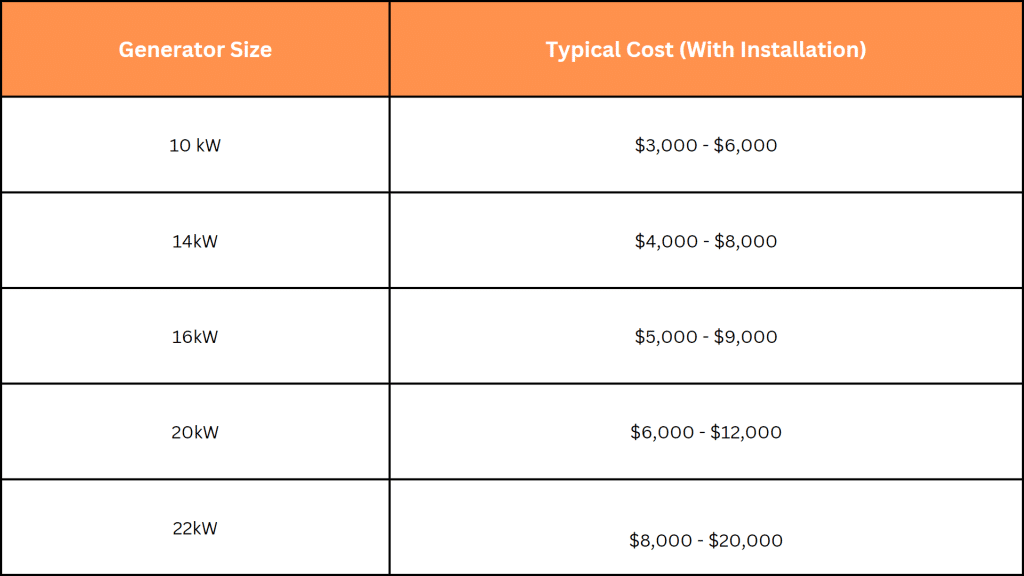

When the storm hits and your lights flicker out, scrambling for backup power is the last thing you need. Many homeowners delay installing a Generac generator simply because of the sticker shock—but that $5,000-$15,000 investment shouldn’t leave you powerless. Generac’s exclusive partnership with Synchrony Financial offers generac generator financing solutions that transform an impossible lump sum into manageable payments. Whether you qualify for interest-free terms or prefer predictable long-term budgeting, this guide cuts through the confusion to show exactly how to secure backup power now without draining your savings.

You’ll discover which financing plan actually saves you money (hint: it’s not always the “0% interest” option), avoid costly mistakes that trigger retroactive interest charges, and learn how to get approved in under a minute. Most importantly, you’ll understand why this isn’t just a one-time loan—but a revolving credit line for all future home projects. Let’s turn power anxiety into peace of mind.

Why Your Generator Payment Is Higher Than Expected

Generac generator financing through Synchrony uses a unique payment structure that catches many homeowners off guard. Unlike standard loans with fixed monthly amounts, both plans calculate payments as a percentage of your highest balance. This means your payment won’t decrease as you pay down the balance—it stays fixed until the debt is cleared.

How Synchrony’s Payment Math Really Works

- 132-month plan: You pay 1.25% of your original balance monthly (e.g., $150/month on a $12,000 generator)

- 18-month plan: You pay 2.5% of your original balance monthly (e.g., $300/month on that same $12,000 unit)

- Critical detail: Payments remain fixed at these amounts even as your balance drops, accelerating payoff but creating higher initial payments than traditional amortized loans

Pro tip: Run your numbers before choosing—on an $8,000 generator, the 18-month plan requires $200/month versus $100/month on the long-term plan. If $200 strains your budget, the fixed 9.99% APR option prevents late fees that could trigger interest penalties.

The $29 Activation Fee Trap

That seemingly small $29 fee gets added to your first statement but doesn’t reduce your required monthly payment. Since payments are based on your highest balance (the original purchase amount), this fee effectively increases your total cost without lowering your obligation. Always factor this into your total cost calculation—especially on smaller purchases under $3,000 where it represents a larger percentage.

18-Month Plan: When “0% Interest” Costs You Hundreds

The interest-free option tempts buyers with “free money,” but Synchrony’s deferred interest model makes it a financial landmine if you miss the deadline. Here’s what dealers won’t emphasize: if you owe even $1 after month 18, you’ll be charged ALL accrued interest from day one of your purchase.

Real-World Cost Comparison

| Scenario | $10,000 Generator Cost | Total Paid (On Time) | Total Paid (Missed Deadline) |

|---|---|---|---|

| 18-Month Plan | $10,000 | $10,000 | $11,498 ($1,498 in retroactive interest) |

| 132-Month Plan | $10,000 | $15,828 | $15,828 (fixed rate) |

Interest calculation: $10,000 at 24.99% APR (standard deferred rate) for 18 months = $1,498

Who Should Actually Choose This Plan

- You can pay the full balance within 15 months (leaving a 3-month buffer)

- Your generator cost is under $5,000 (making $125-$250/month payments manageable)

- You’ve set up automatic payments covering 100% of the balance by month 16

Warning: If your budget is tight, the 132-month plan’s fixed 9.99% APR is safer. That “0% interest” promise becomes your most expensive option the moment life throws a curveball.

Get Approved in 60 Seconds: Your Generac Financing Roadmap

Generac dealers integrate Synchrony’s system directly into their sales process, turning approval into a seamless step—not a barrier. But skipping preparation risks denial or unfavorable terms.

Pre-Check Your Credit Without Damage

Before visiting a dealer, use Generac’s soft-pull pre-qualification tool on their financing page. This reveals:

– Your potential credit limit (no impact on credit score)

– Which plans you’ll likely qualify for

– Valid for 30 days—giving you time to compare dealers

Pro tip: Run this check from home. Dealers see your results too, and knowing your limit helps negotiate better terms or bundle with installation costs.

The 4-Step In-Dealer Application

- Confirm financing capability: Call dealers first—only 60% offer Synchrony financing (filter for “Financing” on Generac’s dealer locator)

- Get a firm quote: Dealers pre-fill your application with the exact generator + installation cost

- Apply instantly: Provide ID and income details; decisions take <60 seconds

- Activate immediately: Use the digital card number for same-day installation scheduling

Critical: Bring proof of income. Synchrony requires annual income verification, and missing this delays approval.

Avoid These 3 Costly Financing Mistakes

Homeowners routinely overpay or trigger penalties by misunderstanding Synchrony’s terms. These pitfalls cost hundreds—or even thousands.

Mistake #1: Ignoring the Revolving Credit Benefit

Closing your Synchrony Project Card after paying off your generator wastes a valuable tool. This isn’t a single-use loan—it’s a dedicated home improvement credit line you can use for:

– HVAC repairs

– Roof replacements

– Future generator upgrades

Leaving it open builds credit history while reserving funds for emergencies.

Mistake #2: Missing Payment Due Dates

Synchrony reports late payments to credit bureaus after 30 days. For the 18-month plan, one late payment risks losing the 0% interest benefit if it pushes your payoff past month 18. Set up automatic ACH payments from your bank account—never rely on manual payments.

Mistake #3: Underestimating Minimum Purchase Rules

Dealers often require $1,500-$3,000 minimum purchases for promotional financing. Smaller accessories (like transfer switches) might not qualify, forcing you to use standard credit card rates (15%-29% APR). Always ask: “What’s the minimum for 0% financing?” before finalizing your order.

Maximize Savings: Timing and Rebates That Slash Costs

Strategic timing and rebates can dramatically reduce your financed amount—meaning lower payments and faster payoff.

Stack Rebates Against Your Balance

- Utility company rebates: Many providers (like PG&E or ConEd) offer $500-$2,000 for generator installations

- State tax credits: Louisiana, Massachusetts, and others provide credits for backup power systems

- Apply as down payment: Direct rebates to your Synchrony balance before financing begins—reducing your principal and monthly payments

Example: A $12,000 generator with a $1,000 utility rebate becomes an $11,000 financed amount, dropping 18-month payments from $300 to $275/month.

Catch Limited-Time Promotions

Dealers occasionally offer extended 0% periods (24-36 months) during storm season or holidays. Ask: “Are there any current financing specials beyond the standard 18 months?” before signing. Synchrony also runs occasional “no activation fee” promotions—saving you the $29 charge.

Manage Payments Like a Pro: Avoid Fees and Build Credit

Your Synchrony account requires active management to prevent fees and leverage long-term benefits.

Payment Method Showdown

| Method | Speed | Fees | Best For |

|---|---|---|---|

| Online ACH | 1-3 days | $0 | All users (set up auto-pay) |

| Phone Payment | Same day | $15 expedited fee | Urgent payments |

| Mail Payment | 7-10 days | $0 | Non-urgent, planned payments |

Critical: Never use phone payments for the 18-month plan’s final payment—mail delays could trigger retroactive interest. Online ACH is the only safe option for deadline-sensitive payments.

Track Your Account Like Your Power Depends On It (It Does)

- Log in to Synchrony Bank’s card services portal weekly during the 18-month plan

- Set calendar alerts for month 16 (payoff deadline)

- Download statements to verify the $29 activation fee wasn’t duplicated

Pro tip: Take a screenshot of your approval screen—your digital card number works for 30 days while waiting for the physical card, enabling immediate installation scheduling.

Your generator financing decision boils down to one question: Can you guarantee paying the full balance within 18 months? If yes, the interest-free plan saves money. If not, the 9.99% fixed-rate plan’s predictable $150/month payment on a $12,000 system prevents financial disasters. Remember: That Synchrony card stays active for future home projects—don’t close it after payoff. Start with Generac’s pre-qualification tool today, then visit a financing-capable dealer. With instant approvals and same-day installation scheduling, backup power could be yours within 72 hours. No more waiting for the “perfect time”—when outages strike, your family’s safety shouldn’t hinge on your savings account balance.